Making Insurance Simple, One Insight at a Time.

Worst Long-Term Care Insurance Companies: Critical 2026 Risks to Avoid

Avoid the worst long-term care insurance companies. Our 2026 guide reveals critical premium risks, claim denial flags, and stable alternative plans.

Quick Summary

Finding the worst long-term care insurers comes down to tracking customer complaints, premium hikes, and claims denials often caused by a provider’s financial instability. To protect your future, you must evaluate a company’s financial strength and satisfaction scores before buying. This educational guide breaks down poorly rated providers’ red flags and explains how to analyze complaints. Note: Our platform offers educational information only; we do not sell insurance products.

Table of Contents

Table of Contents

1. Understanding Long-Term Care Insurance Red Flags

When looking at the market, the phrase “worst long-term care insurance companies” usually points toward carriers exhibiting specific negative traits. The most prominent red flags include exceptionally poor customer service, difficulty in filing claims, and unstable financial backing. If an insurer routinely makes it complicated to access benefits for home health care or nursing facilities, they pose a significant risk to your retirement savings.

If you have ever researched alternative plans, such as those detailed in our guide on LifeX Health Insurance: Critical 2026 Risks & Hidden Plan Rules, you know that navigating the fine print is essential. The same caution applies here. Companies with low ratings from agencies like A.M. Best or Standard and Poor’s should be approached with extreme caution, as low grades indicate a higher risk of the carrier defaulting on their obligations.

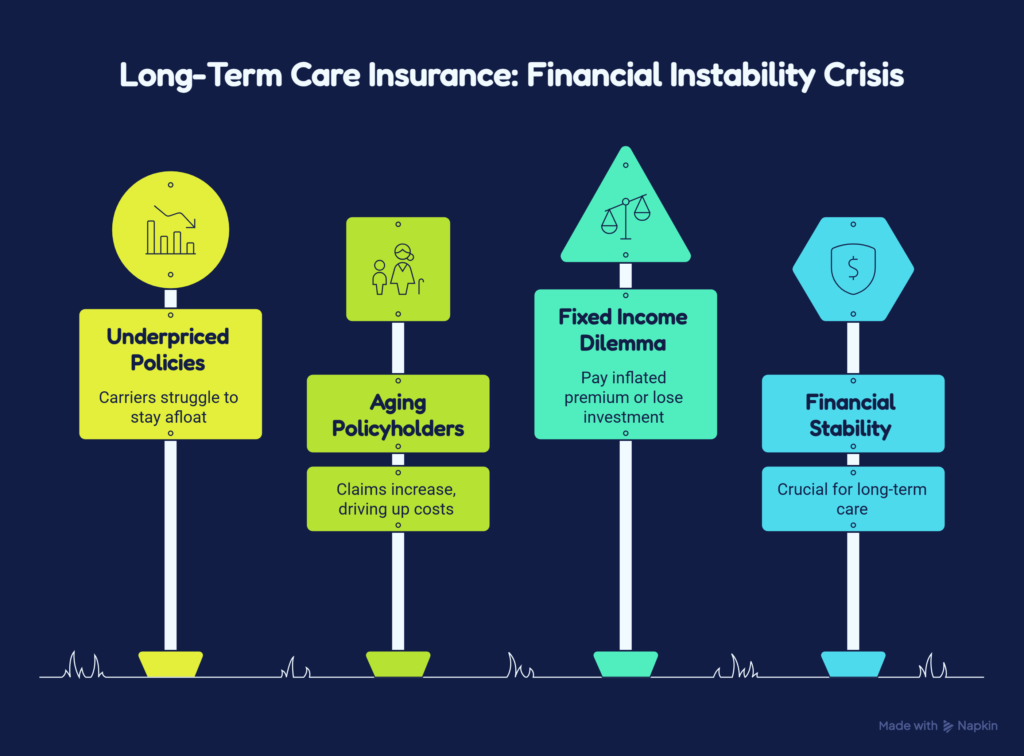

2. High Premium Increases and Financial Instability

One of the main reasons certain providers are labeled among the worst long-term care insurance companies is the shock of sudden, massive rate hikes. Many older policies were underpriced when first sold decades ago. As policyholders aged and claims increased, some carriers had to double or even triple their premiums just to stay afloat.

This creates a terrible dilemma for seniors on a fixed income. They must either pay the inflated premium or drop the policy and lose everything they have invested over the years. Financial stability is paramount. Always check a provider’s multi-year rate increase history before signing a contract.

3. The Problem with Claim Delays and Denials

A cumbersome claims process is a hallmark of a terrible insurance provider. When a family member requires immediate assistance with activities of daily living, waiting months for an approval is unacceptable. Poorly rated companies often demand excessive documentation, repeatedly change their required forms, or deny claims based on technicalities regarding the type of care facility chosen. Reviewing a carrier’s National Association of Insurance Commissioners (NAIC) complaint index can reveal if a company has a higher than average volume of disputes regarding denied benefits.

4. How to Evaluate Provider Ratings and Reviews

To avoid falling victim to a bad policy, you must rely on objective data rather than sales pitches. Look beyond the marketing brochures and check independent rating agencies.

- Financial Strength: An A++ or A+ rating from A.M. Best shows excellent stability. Anything below a B rating is a massive warning sign.

- Customer Satisfaction: Look at J.D. Power studies and Better Business Bureau (BBB) complaints. A pattern of unresolved grievances is a strong indicator of future headaches.

- State Department of Insurance: Local regulators track consumer complaints. If a company has a high complaint ratio in your state, look elsewhere. You can check a company’s official complaint states and consumer data patterns directly through the National Association of Insurance Commissioners Consumer Insurance Search.

5. Alternatives and Hybrid Policies

Because traditional long-term care policies have become expensive and highly unpredictable, many consumers are actively turning to modern alternatives. Relying on legacy contracts often exposes policyholders to the frustrating price spikes associated with the worst long-term care insurance companies. To combat this uncertainty, the insurance market has developed innovative products that offer more stability and dual benefits.

The Rise of Hybrid Life Insurance Policies

Hybrid life insurance combines permanent coverage with a long-term care rider, allowing you to accelerate your death benefit to pay for nursing or in-home care. To understand how these modern frameworks protect your family, read our Open Care Life Insurance: 2026 Guide to Costs, Policies, and Reviews. If you never need care, the policy simply pays a tax-free death benefit to your heirs—completely eliminating the “use it or lose it” risk of standalone policies.

Annuities with Long-Term Care Riders

For individuals who have a lump sum of savings and want to protect it from market volatility while securing future health needs, annuities with long-term care riders present a fantastic option. You deposit a single premium, and the insurance company guarantees a specific pool of money dedicated specifically for long-term care expenses. Similar to hybrid life policies, these options typically offer a guaranteed premium structure, meaning you will never receive a sudden notice in the mail demanding double the payments just to keep your coverage active.

Short-Term Care and Self-Funding Strategies

If age or health conditions disqualify you from traditional or hybrid policies, short-term care insurance serves as a viable backup plan. These policies provide up to 360 days of coverage with much easier underwriting requirements. Additionally, some families choose to self-fund their long-term care by heavily investing in Health Savings Accounts (HSAs) or setting aside dedicated real estate investments. By exploring these diverse avenues, you can bypass the worst long-term care insurance companies entirely and build a customized, secure safety net for your future.

6. Frequently Asked Questions (FAQs)

What makes a long-term care insurance company bad?

A bad company is typically characterized by a history of massive premium rate increases, poor financial stability, unresponsive customer service, and a high rate of claim denials.

How can I check a company’s complaint record?

You can view a company’s complaint index through the National Association of Insurance Commissioners (NAIC) website or by contacting your state’s department of insurance directly.

Why do long-term care premiums increase so much?

Many legacy policies were priced before insurers accurately understood the true cost of modern extended medical care and life expectancy. To avoid bankruptcy, many companies legally petitioned state regulators to raise rates on existing policyholders.

Are hybrid long-term care policies better?

For many people, yes. Hybrid policies combine life insurance with long-term care benefits. They usually feature locked in premium rates and guarantee a payout either for care or as a death benefit, making them less risky than traditional standalone policies.

What happens if my insurance company goes bankrupt?

If your carrier becomes insolvent, state guaranty associations will typically step in to cover your claims up to a certain legal limit. However, the process can cause severe delays and added stress, which is why choosing a highly rated company initially is vital.

7. Conclusion

Avoiding the worst long-term care insurance companies requires diligence, research, and a clear understanding of your financial goals. By paying close attention to financial strength ratings, tracking consumer complaints, and watching out for histories of extreme premium hikes, you can protect your retirement assets. Whether you opt for a traditional standalone policy or a modern hybrid plan, always ensure the company backing your contract has a proven track record of honoring their commitments.

Read More:

(Disclaimer: This article is strictly for educational and informational purposes. We do not sell insurance products or provide financial advice. Always consult with a licensed insurance broker or a certified financial planner before making any decisions regarding long-term care coverage.)