Making Insurance Simple, One Insight at a Time.

Open Care Life Insurance: 2026 Guide to Costs, Policies, and Reviews

Explore Open Care life insurance costs per month and specialized final expense policies for seniors. Read essential customer reviews and BBB ratings to find the best life insurance coverage to protect your family’s financial future.

Quick Summary

Open Care Life Insurance provides financial security through senior-focused products, including term, whole life, and final expense policies. Monthly premiums fluctuate based on factors like age and health, with common coverage options typically ranging from $10,000 to $300,000. To ensure a reliable experience, it is vital to research customer feedback, specific complaints, and Better Business Bureau (BBB) ratings before selecting a plan. This informational guide is designed to help you navigate these insurance choices without serving as a direct provider.

Table of Contents

Table of Contents

1. Understanding Open Care Life Insurance

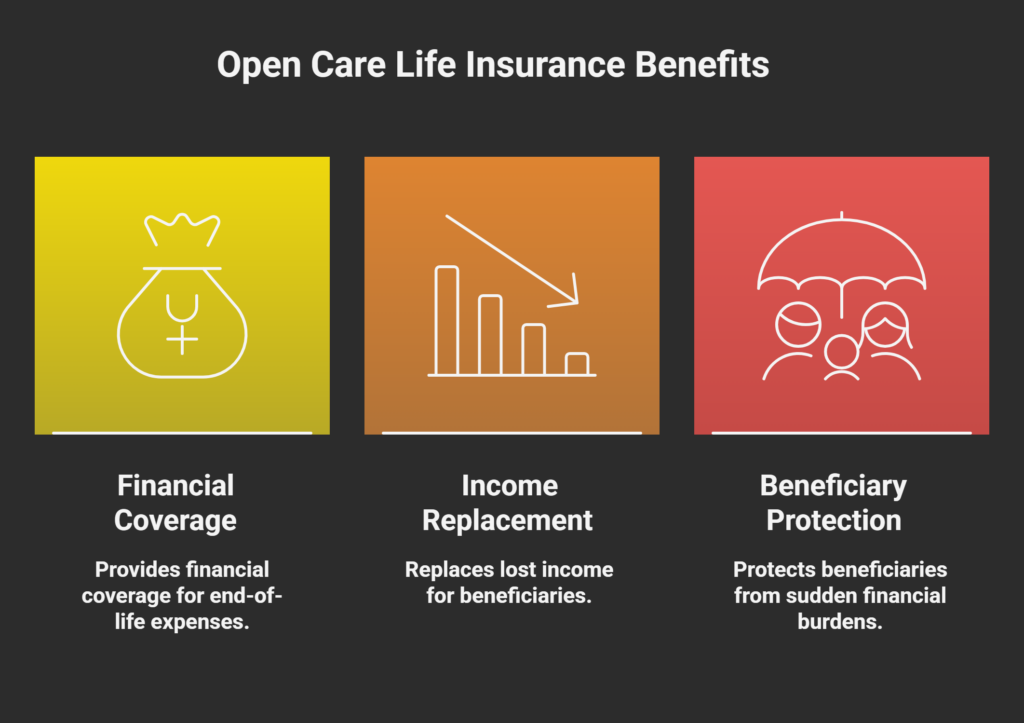

When planning for the future, finding the right safety net for your loved ones is crucial. At its core, Open Care provides policyholders with financial coverage designed to handle end-of-life expenses, replace lost income, and protect beneficiaries from sudden financial burdens.

One important distinction worth understanding from the outset is that Open Care is an insurance marketing organization (IMO), not a direct insurance carrier. When you purchase a policy through Open Care, your actual contract and claims are handled by one of their carrier partners, which in 2026 include companies such as Mutual of Omaha, Aetna, Transamerica, and Foresters Financial. Understanding this distinction helps you know exactly who you are dealing with when it comes to policy servicing and claim payouts.

For a broader foundation on how life insurance works before diving into Open Care specifically, our Frequently Asked Questions page covers the most common questions Americans ask about life insurance types, costs, and coverage decisions.

Eligibility and Application

Eligibility criteria for Open Care life insurance typically depend on the specific policy you choose. While term policies might require health questions, final expense options generally offer guaranteed or simplified issue features, making them highly accessible for seniors. Knowing how to apply usually involves requesting a quote online, answering a brief health questionnaire, or calling the Open Care phone number to speak directly with an agent.

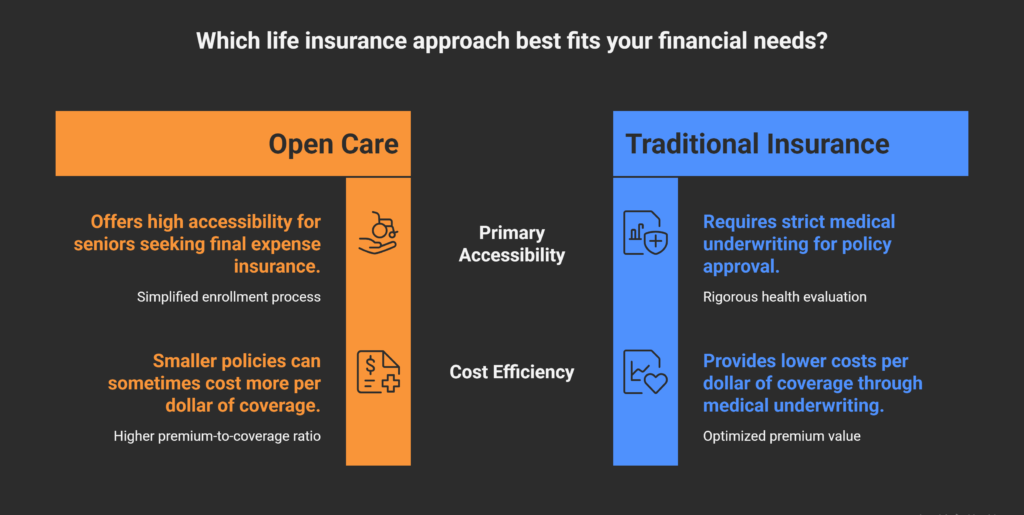

Open Care vs. Traditional Life Insurance

Compared to traditional life insurance which might involve strict medical underwriting and lengthy approval times. Open Care Open Care life insurance often focuses on streamlined processing, particularly for its senior demographic. The primary benefits include faster approval times and specialized final expense coverage.

2. Types of Open Care Life Insurance Policies

When navigating the Open Care Open Care life insurance network, you will find several ways to customize an Open Care life insurance policy to fit your specific needs. It’s important to understand the broader context – many people ask, what are the 4 types of life insurance? Generally, these are Term, Whole, Universal, and Variable. Open Care life insurance focuses primarily on the following:

- Term Life Insurance under Open Care: This provides coverage for a specific period (e.g., 10, 20, or 30 years). It is an excellent, budget-friendly option for replacing income during your prime working years.

- Whole Life Insurance under Open Care: This permanent policy covers you for your entire lifetime as long as premiums are paid. For those who also own vehicles or motorcycles, understanding your short term coverage options is equally important. Our One Day Bike Insurance guide covers temporary motorcycle protection for riders who do not need a full annual policy. It also builds cash value over time.

- Open Care Final Expense Life Insurance: Often heavily marketed toward older adults, this is a smaller whole life policy (often around $10,000 to $25,000) designed specifically to cover funeral costs, medical bills, and other end-of-life debts.

- Critical Illness Coverage: Some Open Care policies offer riders or built-in benefits that allow you to access a portion of your death benefit early if you are diagnosed with a qualifying critical illness.

3. Breaking Down Costs and Premiums

One of the most heavily searched topics is the Open Care life insurance cost per month. Pricing is rarely one-size-fits-all.

Factors Affecting Premiums

Your monthly rates will depend on your age, gender, tobacco use, overall health, and the type of policy you select. Guaranteed issue plans, which require no health questions, typically cost 20 to 30 percent more than simplified issue plans that do involve basic health screening. This premium difference reflects the higher risk the insurer accepts by covering all applicants regardless of health status.

Open Care Rates for Seniors

Because older applicants represent a higher risk to insurers, senior-focused life insurance policies typically carry higher premiums than policies issued to younger applicants. It is worth noting that while Open Care life insurance advertises plans starting at very low monthly rates in its television commercials, actual premiums for most seniors will be higher depending on age, gender, and coverage amount. Always request a personalized quote rather than relying on advertised starting prices. The Federal Trade Commission (FTC) provides useful guidance on understanding insurance advertising and what to watch for when evaluating policy offers.

Payment Options

Ask about payment flexibility when requesting a quote. In some cases, paying annually rather than monthly can unlock modest discounts on your overall premium cost.

Real-World Pricing Benchmarks

How much is a $10,000 life insurance policy? For a healthy individual in their 50s or 60s, a $10,000 final expense policy can range from $30 to $80 per month depending on the provider and the applicant’s health profile.

How much life insurance can you get for $9.95 a month? This is a popular unit-based pricing model frequently advertised on television. For a senior, $9.95 typically buys only a small fraction of coverage, often just a few hundred to a couple of thousand dollars, depending on age and the specific policy structure.

How much does a $100,000 whole life insurance policy cost per month? Whole life is significantly more expensive than term coverage. A $100,000 whole life policy could cost anywhere from $100 to over $400 monthly, heavily dependent on the applicant’s age at the time of issuance.

4. The Claims Process and Maximizing Benefits

Understanding the claims process for Open Care life insurance is just as important as buying the policy.

How to File a Claim

To file a claim through Open Care’s carrier partners, beneficiaries typically need to submit a certified death certificate and complete the carrier’s specific claim forms. Because Open Care is a marketing organization rather than a direct carrier, it is important to identify which carrier issued your specific policy and contact that carrier directly for claims processing. Initiating this process promptly helps ensure a smoother and faster payout experience.

Graded Benefit and Waiting Periods

A critical detail to understand when evaluating any guaranteed issue final expense policy is the graded benefit structure. Many guaranteed issue plans include a two-year waiting period during which the full death benefit is not immediately payable. If the insured passes away within the first two years of the policy, beneficiaries typically receive a return of premiums paid plus interest rather than the full face value. Always confirm whether a policy has a waiting period before purchasing.

Common Reasons for Claim Denials

To maximize your benefits you must be aware of why a company might refuse a payout. Most policies will not pay out if the insured commits suicide within the first two years of the policy, which is known as the contestability or suicide clause. Additionally, if the policyholder provided false information on their application, known as material misrepresentation, or died while committing a felony, the claim may be denied. Being fully truthful on your application is the single most important step you can take to protect your beneficiaries.

5. Open Care Life Insurance Reviews and Reputation

Before committing to any financial product, investigating Open Care life insurance reviews is a mandatory step.

Pros and Cons

Choosing Open Care life insurance offers the advantage of accessibility, especially for seniors seeking final expense coverage who may have been declined elsewhere due to health conditions. The tradeoff is that guaranteed issue policies, which accept all applicants regardless of health, typically cost more per dollar of coverage compared to medically underwritten policies available through other carriers.

Customer Feedback and Complaints

Reviewing Open Care life insurance complaints reveals that the most common grievances from customers center on high volumes of direct mail marketing and unsolicited phone calls rather than issues with policy performance or claim denials. Consumers have reported receiving multiple mailers per month and frequent telemarketing contacts after requesting a quote. These are legitimate concerns about marketing practices, but they are distinct from concerns about the quality of the actual insurance products offered through their carrier partners.

Reputation and Ratings

When evaluating any insurance provider, always look up their Better Business Bureau profile for a clear picture of how the company handles and resolves customer grievances. The Better Business Bureau maintains publicly accessible business profiles and complaint histories that allow consumers to make more informed decisions before purchasing financial products. Also consider looking up the financial strength ratings of the actual carrier issuing your policy, such as Mutual of Omaha or Transamerica, through independent rating agencies like A.M. Best.

6. Global Perspectives: Life Insurance Beyond Open Care

Comparative Perspectives: Life Insurance in the United States

While Open Care life insurance serves a specialized niche in the market, it is part of a highly competitive US life insurance landscape. American families frequently compare these offerings against other national providers to ensure they are securing the best value for their budget. Search trends across the United States show high demand for specific coverage benchmarks, with many seniors prioritizing a $25,000 policy to manage final expenses, while others with broader protection needs focus on larger coverage amounts such as $500,000 whole life policies.

Whether you are exploring Open Care life insurance for its no-exam pathways or comparing it against other carriers, the core goal remains consistent: finding a reliable and affordable plan to protect your family’s financial future. For additional guidance on what to look for when evaluating any life insurance provider, the National Association of Insurance Commissioners (NAIC) provides a free consumer information center where you can research carriers, verify licenses, and access complaint data for any insurance company operating in your state. Understanding how your life insurance decisions fit into your broader financial picture, including your health coverage, home protection, and legal documentation, is something we cover in depth across our About Us page, where you can learn more about the editorial mission behind Insuria Insights.

7. Frequently Asked Questions

What are the main benefits of life insurance?

Life insurance provides financial security for your beneficiaries, peace of mind knowing your loved ones are protected, risk mitigation against sudden income loss, and in the case of whole life policies, a potential vehicle for tax-advantaged cash value accumulation over time.

What are the seven main types of insurance?

The core types of insurance most individuals and families need include life insurance, health insurance, auto insurance, homeowners insurance, renters insurance, disability insurance, and long-term care insurance.

What are five disadvantages of life insurance?

It can represent a significant ongoing monthly cost. Complex policy terms and hidden clauses can confuse buyers. Claims can be denied if exact policy conditions are not met. Term policies offer no return on premiums if you outlive the coverage period. Some inflexible policies may not adapt well to major life changes such as divorce or the death of a named beneficiary.

What is the minimum cost of health insurance per month?

While this guide focuses on life insurance, minimum health insurance costs vary significantly by state, income level, employer contributions, and available subsidies. Some state-sponsored Medicaid plans can be available at no cost for qualifying low-income individuals, while standard private minimum-coverage plans often start around $200 to $300 monthly for an individual.

What is the 7-year rule for life insurance?

The 7-year rule relates to the Modified Endowment Contract (MEC) limits set by the IRS. It states that if total premiums paid into a life insurance policy within the first seven years exceed the amount needed to provide a paid-up policy, the policy loses certain tax advantages and distributions may be treated differently for tax purposes.

How much does a $300,000 life insurance policy cost per month?

For a healthy 30-year-old, a 20-year term policy for $300,000 might cost as little as $15 to $25 per month. For a whole life policy of the same face value, that monthly cost could rise to several hundred dollars depending on the applicant’s age and health at the time of issuance.

What does third-party insurance mean?

Third-party insurance, most commonly referenced in the context of auto insurance, refers to coverage that pays for damages or injuries caused to another party in an accident where you are at fault. It covers the other party’s losses but does not cover damage to your own vehicle or injuries to yourself.

8. Conclusion

Securing the right life insurance policy is one of the most meaningful ways to protect your loved ones from financial hardship. Whether you are exploring Open Care life insurance final expense coverage, analyzing monthly costs for senior plans, or comparing a standard term policy against whole life options, the key is thorough and patient research.

Always review Open Care life insurance feedback carefully, understand the graded benefit waiting period if applicable, verify which carrier is actually issuing your policy, and accurately calculate the amount of coverage your family truly needs. By understanding the full range of options available, from a modest $10,000 final expense policy to more robust whole life plans, you can make an educated and confident decision that serves your family well for years to come.

(Disclaimer: This blog post is intended for informational and educational purposes only and does not constitute financial, legal, or insurance advice. Always consult with a licensed insurance agent before purchasing a policy.)