Making Insurance Simple, One Insight at a Time.

Balance Care Insurance Explained: Reviews, Costs and Coverage Guide

Wondering what balance care insurance covers? Explore our comprehensive guide on balance care health insurance reviews, costs, multi plan networks, and pros or cons.

Quick Summary

Welcome to Insuria insights, your go-to educational platform for navigating the complex healthcare market. While we do not sell policies directly, this guide breaks down everything you need to know about it. From understanding costs, multi plan networks, and coverage for pre-existing conditions, to comparing these plans with traditional Obamacare, we have you covered. Keep reading to explore the pros and cons, learn how to evaluate providers, and discover how to choose the perfect policy for your medical and financial needs.

Table of Contents

Table of Contents

1. Balance Care Insurance Overview

What is Balance Care Insurance?

Because the healthcare market is so diverse, many people frequently ask, “what is balance care health insurance?” Depending on your state, it generally refers to a flexible health plan model, a regional insurance brokerage, or a customized network of supplemental benefits. The core goal of these plans is to provide a sensible middle ground between high-deductible catastrophic coverage and highly expensive, top-tier comprehensive plans.

Key Features of Balance Care Insurance

The standout features of these plans often include access to extensive provider networks, built-in wellness programs, and valuable supplemental coverage. For example, a well-rounded policy will often include this, vision and dental benefits alongside your standard doctor visits and preventative care.

Balance Care Insurance vs. Traditional Insurance

Traditional insurance policies often come with very rigid structures and strict network limitations. In contrast, balanced healthcare models aim to offer more flexibility when it comes to choosing out-of-pocket limits. If you are investigating non-traditional healthcare options outside the standard state marketplace, it helps to understand alternative corporate frameworks like the one detailed in our guide to LifeX Health Insurance: Critical 2026 Risks & Hidden Plan Rules. Consumers frequently compare these alternative models with standard Obamacare plans to see which option provides better monthly subsidies and lower deductibles.

Benefits of Balance Care Insurance

What are the benefits of this insurance? Primarily, it provides policyholders with a tailored safety net. It protects your personal finances from medical debt while ensuring you have access to quality doctors. Many families find that having this type of balance protection insurance is worth it simply for the peace of mind it brings during unexpected medical emergencies.

How to Choose the Right Balance Care Insurance Plan

Selecting the right plan requires a careful look at your medical history, your monthly budget, and your local hospital networks. Always verify that your preferred primary care physicians are in-network and take the time to read the summary of benefits carefully.

2. How Balance Care Insurance Works

Understanding the Balance Care Insurance Model

The underlying model operates by pooling member resources to negotiate lower rates with healthcare facilities. Many of these plans utilize wide-reaching networks, such as the balance care multiplan, to ensure members can find a doctor no matter where they travel domestically.

Who Needs Balance Care Insurance?

This type of coverage is ideal for individuals seeking flexible or supplemental medical coverage. Independent contractors, early retirees, and families wanting a blend of affordability and comprehensive care are usually the best candidates for this model.

Examples of Balance Care Insurance in Practice

A healthy individual might use this insurance strictly to cover routine checkups and wellness visits while keeping their monthly premiums low. Another example involves members utilizing the balance care insurance unified caring association benefits to get discounts on alternative wellness therapies, prescription drugs, and lifestyle services.

Financial Structure of Balance Care Insurance

Premiums, deductibles, and co-pays are carefully structured to prevent catastrophic financial loss. Sometimes younger, healthy individuals wonder, “Is it actually cheaper to not have health insurance?” The answer is almost always no. A single emergency room visit or sudden illness can cost tens of thousands of dollars, making a monthly premium a far safer and smarter financial strategy.

Scenarios Where Balance Care Insurance is Beneficial

If you need specialized care but do not want to pay the massive premiums associated with platinum-tier traditional plans, a balanced approach can cover your specific needs without forcing you to pay for unnecessary policy riders.

3. Balance Care Insurance Providers

Top Balance Care Insurance Companies

When searching for a reliable provider, many consumers ask, “Is balance a good company?” or “Is Balanced Healthcare legit?” Yes, established entities operating under these names are legitimate and regulated, though the quality of coverage can vary by state. Consumers also frequently ask, “Is balance care ambetter?” While they are distinct entities, both companies operate in the affordable health plan space. If you are researching the “what is the top 5 best health insurance?” list, you will typically find major national carriers alongside these specialized regional balanced care providers.

How to Evaluate a Balance Care Insurance Provider

You should always evaluate a provider based on their financial stability ratings, their network size, and the quality of their customer support. Reading independent balance care insurance reviews is an excellent starting point for your research.

Customer Reviews of Balance Care Insurance Providers

Do not rely solely on a company’s marketing materials. Searching for balance care insurance reviews bbb or balance care insurance reviews yelp can give you a highly realistic picture of how a company handles claim disputes, billing errors, and customer service calls. Furthermore, you might want to look up balance care multiplan reviews if your specific policy utilizes that secondary provider network.

Balance Care Insurance Providers by Region

Healthcare is highly localized, meaning plan availability varies greatly. For instance, balance care insurance florida might offer completely different benefits, networks, and pricing structures compared to plans offered in Texas or California.

How to Contact Balance Care Insurance Providers

If you need to speak with a representative, you can usually reach out via the specific balance care insurance provider phone number or the general toll-free balance care insurance phone number listed on their official website. For existing policyholders, utilizing the balance care – insurance provider portal or the balance care – insurance login page is the fastest way to check your claims, get support, or locate the correct balance care insurance billing address.

4. Applying for Balance Care Insurance

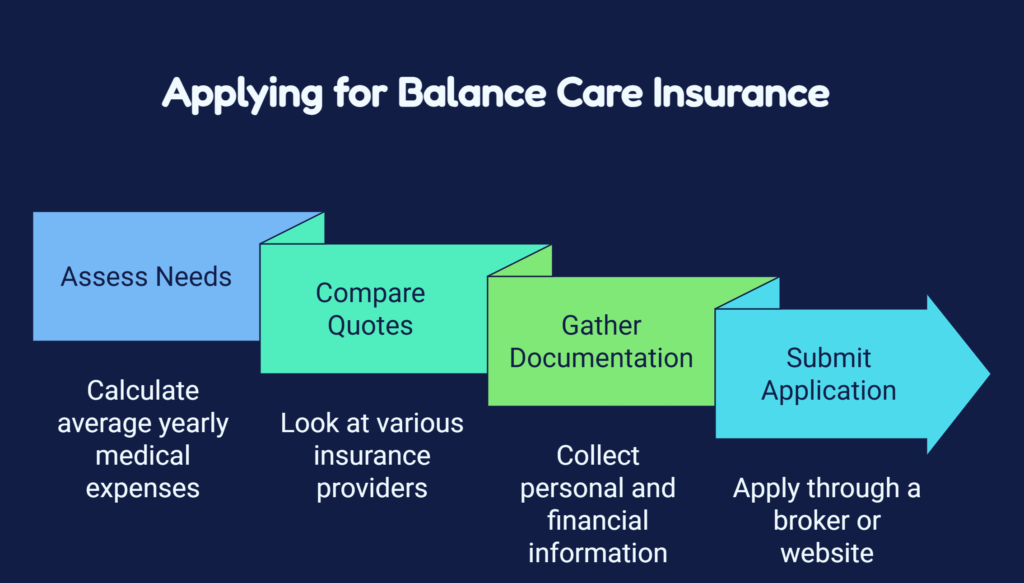

Step-by-step Guide to Applying for Balance Care Insurance

- Assess your needs: Calculate your average yearly medical expenses.

- Compare quotes: Look at various balance care insurance providers.

- Gather documentation: Collect your personal and financial information.

- Submit application: Apply through a licensed broker or the official provider website.

Documents Needed for Balance Care Insurance Application

You will typically need a valid government ID, proof of current address, recent tax returns (if you are applying for government subsidies), and social security numbers for all dependents you wish to cover.

Common Mistakes When Applying for Balance Care Insurance

Skipping the fine print is a major error. Additionally, failing to understand the exact process of how to cancel balance care insurance if you eventually find a better plan can lock you into an unwanted contract. Always know your exit options.

How to Compare Balance Care Insurance Quotes

When looking at quotes, do not just focus on the lowest monthly premium. You must compare the out-of-pocket maximums, the deductible amounts, and the co-pays for specialist visits to get a true picture of the plan’s value.

Frequently Asked Questions About Balance Care Insurance Application

During the application phase, users often have highly specific questions regarding eligibility, effective dates, and network restrictions. We have compiled the most common inquiries in the dedicated FAQ section below.

5. Frequently Asked Questions (FAQs)

Is Balance Care a real insurance company?

Yes. Depending on your location, Balance Care operates either as a regional health maintenance organization (HMO), an independent insurance brokerage, or a provider of supplemental health and wellness benefits.

How much does balance care health insurance cost?

Costs fluctuate widely based on your age, zip code, and the tier of the plan you choose. A basic individual plan might cost a few hundred dollars a month, whereas comprehensive family plans will be notably higher.

What does balance care cover?

While policies vary, they typically cover preventative care, standard doctor visits, hospital stays, and emergency services. Many plans also integrate supplemental vision and dental care.

Can a diabetic get health insurance?

Absolutely. Under current federal healthcare laws, insurance companies cannot deny you coverage or charge you more simply because you have a pre-existing condition like diabetes. You can review the full legal protections and marketplace rights directly on HealthCare.gov.

Is autoimmune disease covered by insurance?

Yes, standard health insurance plans cover the medical treatments and doctor visits associated with autoimmune diseases. However, specific coverage for specialty medications will depend entirely on your plan’s drug formulary.

Is Parkinson’s disease covered by health insurance?

Yes, regular health insurance covers the standard medical and clinical treatments for Parkinson’s disease.

Can you get long-term care insurance with Parkinson’s?

This is a different scenario. While regular health insurance covers the medical treatment, getting a new long-term care insurance policy after receiving a Parkinson’s diagnosis is incredibly difficult, and most applications will be denied. It is crucial to secure long-term care policies before major health issues arise.

What does Dave Ramsey recommend for health insurance?

Financial expert Dave Ramsey generally recommends purchasing a High Deductible Health Plan (HDHP) and pairing it with a Health Savings Account (HSA) if you are in good health, as this allows you to save money tax-free for medical expenses.

What does Dave Ramsey say about LTC insurance?

When it comes to long-term care (LTC) insurance, Dave Ramsey strongly advises purchasing a policy on your 60th birthday to protect your retirement nest egg from the astronomical costs of nursing home care. However, because many legacy carriers face financial instability and rising consumer complaints, we highly recommend checking our report on the worst long-term care insurance companies before locking yourself into a permanent premium plan.

Who has the best Medicare plan for seniors?

There is no single “best” plan for everyone. The right Medicare plan depends entirely on your specific prescription drug needs, your preferred doctors, and your budget. Seniors should compare Medicare Advantage and Medicare Supplement plans every year during the open enrollment period.

6. Conclusion

Finding the right healthcare coverage does not have to be an overwhelming process. By understanding the core features of this insurance, you can make an informed decision that protects your health and your wallet. Always take the time to compare multiple balance care insurance providers, read independent reviews, and verify that your favorite doctors are in-network before signing any contracts. Remember, as an informational platform, Insuria insights is here to provide you with the educational tools you need to navigate the market confidently. We highly encourage you to consult with a licensed, independent insurance broker in your state to discuss your specific medical needs and find the perfect plan for you and your family.