Making Insurance Simple, One Insight at a Time.

Denied Payout? How a Life Insurance Lawyer Can Save Your Claim

Facing a delayed or denied claim? Learn how a life insurance lawyer protects your beneficiary rights, navigates legal disputes, and secures your payout.

Quick Summary

When a life insurance company delays, minimizes, or flat-out denies a claim, it can leave families facing severe financial stress during a time of grief. A specialized life insurance lawyer helps beneficiaries navigate these complex legal roadblocks, challenge unfair denials, and fight to secure the payout they are rightfully owed. This guide breaks down common policy disputes, what to expect regarding attorney fees, how to find the right legal help across different regions, and what steps you can take today to protect your rights.

Table of Contents

Table of Contents

- Understanding Life Insurance Legal Issues

- Under What Circumstances Will Life Insurance Not Pay?

- How to Choose a Life Insurance Lawyer

- Understanding Lawyer Costs and Consultations

- Filing a Life Insurance Claim with Legal Help

- Legal Considerations for Beneficiaries

- Frequently Asked Questions (FAQs)

- Conclusion

Understanding Life Insurance Legal Issues

The framework for managing life insurance disputes involves a deep dive into contractual obligations. Understanding life insurance legal issues requires navigating complex policy terms, identifying common disputes, and recognizing the direct role of attorneys in resolving life insurance cases.

| UNDERSTANDING LIFE INSURANCE LEGAL ISSUES | |

|---|---|

| Core Focus Area | Key Legal Components |

| Common Disputes in Claims | Material Misrepresentation Exclusions & Suicide Clauses |

| Challenging a Policy Denial | Administrative Appeals Bad Faith Lawsuits |

| Policy Term Interpretation | Ambiguous Language Clauses Grace Period Protections |

Insurance contracts are dense documents filled with legal jargon. When a claim is filed, insurance companies review the initial application details with a fine-tooth comb. A dispute typically arises when the carrier claims that the policyholder did not disclose a pre-existing condition or failed to keep up with premium payments. If you encounter difficulties tracking down the historical documentation for an older policy during a dispute, reviewing an entry like our Great Western Insurance Company Review can offer helpful perspective on tracing legacy policy details and finding carrier contact routes.

Under What Circumstances Will Life Insurance Not Pay?

Many policyholders and beneficiaries wonder about the exact boundaries of life insurance coverage. Medical history queries frequently impact coverage validity and claim approvals. Important questions include whether you can get life insurance with lupus, if a person with dementia can get life insurance, or if someone with a pacemaker can get life insurance.

Carriers evaluate these conditions during underwriting. If a condition is fully disclosed, the policy should pay out upon the insured’s passing. However, under what circumstances will life insurance not pay?

- The Contestability Period:

If the policyholder passes away within the first two years of the policy being active, the insurance company has a legal right to investigate the original application for inaccuracies.

- Material Misrepresentation:

If an individual failed to mention a critical diagnosis (such as advanced dementia, active lupus complications, or recent pacemaker surgeries) during application underwriting, the company may void the policy and deny the claim.

- Policy Disqualifications:

Standard policy exclusions can include hazardous hobbies, aviation accidents, or suicide clauses within the initial contestability window.

If you are looking to round out your asset protection strategies beyond life insurance, you can explore specialized asset rules in our comprehensive Custom Motorcycle Insurance Guide to learn how distinct policy exclusions operate in alternative coverage markets.

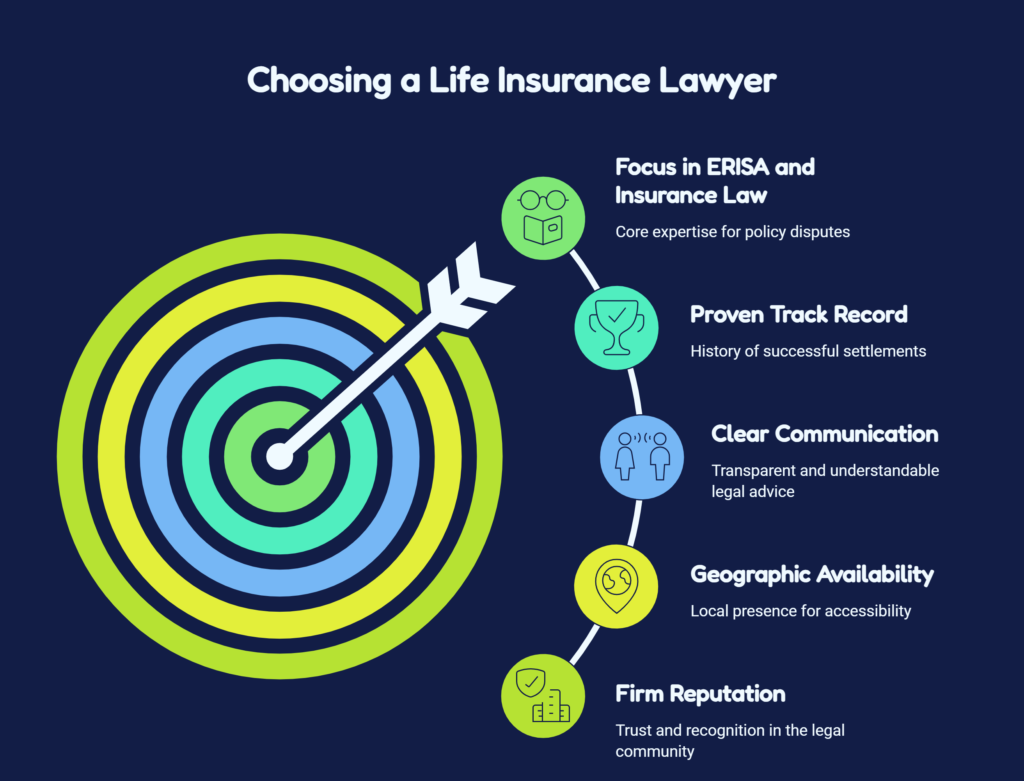

How to Choose a Life Insurance Lawyer

Selecting the right legal advocate requires evaluating experience, geographic availability, and specific firm reputations. When we look at regional searches across search platforms, many beneficiaries look for a life insurance lawyer near me or target regional experts like a life insurance lawyer Florida, life insurance lawyer California, life insurance lawyer Alabama, life insurance lawyer Nj, life insurance lawyer new York, life insurance lawyer Arizona, or life insurance lawyer Pennsylvania.

The broader market search trends show that consumers often seek out specific recognized groups, such as The Lassen Law Firm, alongside evaluating the best legal insurance plans for individuals or researching solo attorney malpractice insurance cost details.

When choosing an attorney to challenge an insurance denial, prioritize these core qualities:

- Focus in ERISA and Insurance Law:

Group life insurance policies provided by employers are governed by a complex federal law called ERISA, which requires highly specialized administrative appeal strategies. Independent policies are governed by state law.

- Proven Track Record:

Look for client testimonials and verifiable reviews indicating a strong history of winning policy settlements against major carriers.

- Clear Communication:

A good lawyer will layout realistic timelines and avoid confusing legal terminology.

Understanding Lawyer Costs and Consultations

The financial aspect of hiring legal representation is a primary concern for grieving families. Common user queries emphasize looking for a life insurance lawyer free consultation, an insurance lawyer free consultation near me, or a life insurance attorney free consultation to assess the viability of a case without upfront costs.

How Much Does an Insurance Lawyer Cost?

Most life insurance lawyers work on a contingency fee basis. This means they do not charge any upfront fees or hourly rates. Instead, they receive a fixed percentage (typically between 25% and 40%) of the final settlement or court award. If they do not win your case, you do not owe them an attorney fee.

Navigating the interactive data shows that people often worry about how to get an attorney if I have no money or whether they can get a lawyer and pay later. The contingency fee model directly solves this issue, allowing low-income individuals to access high-quality representation.

What Happens at a Free Lawyer Consultation?

During your initial free consultation, the attorney will review the insurer’s denial letter, analyze the original policy language, and determine if the carrier acted in bad faith. This meeting is entirely exploratory and does not obligate you to sign a contract.

Filing a Life Insurance Claim with Legal Help

Filing a claim properly from day one minimizes the chances of a lengthy dispute. If an insurer delays or rejects your claim, a lawyer can step in to manage all correspondence with the insurance adjuster.

Crucial Tip for Beneficiaries:

Be highly mindful of what not to say to the insurance adjuster. Avoid speculating on medical timelines, admitting to unverified health issues of the deceased, or agreeing to recorded statements without legal counsel present.

An attorney helps gather the exact documentation needed for complex claims, such as independent medical evaluations, autopsy report clarifications, and certified premium payment histories. They ensure that your response to a claim review process satisfies all statutory deadlines, effectively mitigating intentional stalling tactics by the carrier.

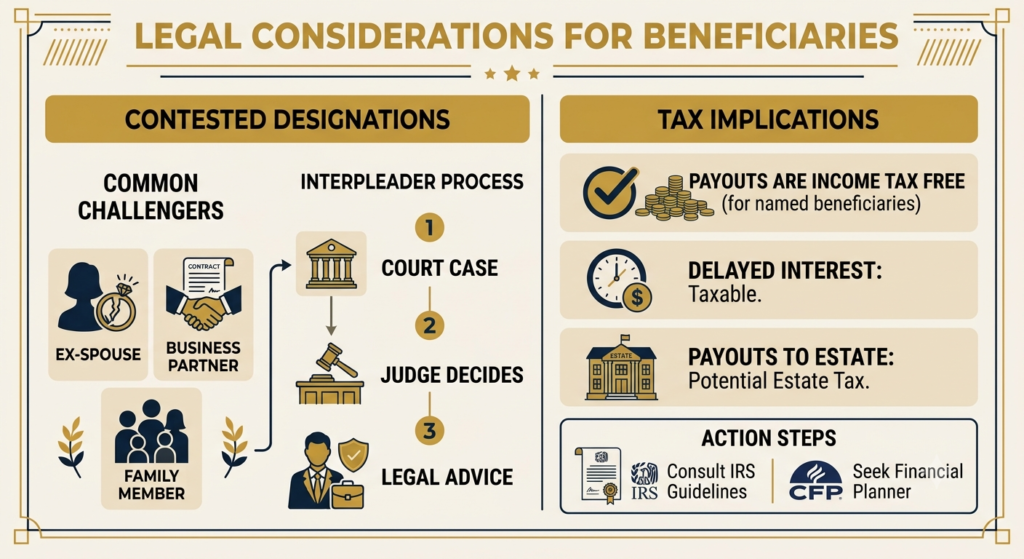

Legal Considerations for Beneficiaries

Beneficiaries hold distinct legal rights that protect them from unfair carrier corporate policies. These rights encompass handling contested beneficiary designations, managing changing a life insurance beneficiary legally, and understanding tax implications.

- Contested Beneficiary Designations:

If an ex-spouse, business partner, or family member challenges your right to a payout, the insurance company may file an “interpleader action.” This places the funds in the custody of a court while a judge decides who legally deserves the money. A life insurance lawyer is vital to representing your interests during an interpleader lawsuit.

- Tax Implications:

Generally, life insurance payouts are completely free of federal income tax when distributed to a named beneficiary. However, interest accrued on delayed payouts may be taxable, and major payouts distributed to an estate rather than a person could impact estate tax calculations. You can check the definitive tax guidelines directly through the official Internal Revenue Service (IRS) or consult a certified financial planner.

Frequently Asked Questions (FAQs)

Can you sue a life insurance policy?

Yes. If an insurance company denies a valid claim or engages in bad faith practices (such as stalling a payout without a legitimate reason), you have the legal right to sue the insurance company for breach of contract.

What not to tell the attorney?

You should never hide facts or lie to your attorney. Attorney-client privilege protects your conversations. Hiding a pre-existing medical condition or an issue with premium payments only prevents your lawyer from building a proper strategy to counter the insurance company’s arguments.

Can I call a lawyer to ask questions for free?

Yes. Most life insurance attorneys provide a free initial consultation to review your claim denial letter and explain your legal options without any financial obligation.

What is the maximum income to qualify for legal aid?

Legal aid qualifications vary significantly by state and local jurisdiction, often requiring an applicant’s income to fall below 125% to 200% of the federal poverty guidelines. However, because most life insurance lawyers work on a contingency fee basis (taking a percentage of the payout only if they win), you can typically secure private representation regardless of your current income status.

What are red flags for lawyers?

When hiring an attorney, look out for warning signs such as a lack of transparency regarding fee structures, unreturned phone calls, guarantees of a specific settlement amount, or an absence of experience focusing specifically on life insurance or ERISA law.

Conclusion

Navigating a life insurance claim denial can feel overwhelming, but you do not have to face corporate insurance adjusters alone. By understanding your policy terms, recognizing when a carrier is acting in bad faith, and leveraging a life insurance lawyer through a free consultation, you can balance the scales of justice. Securing professional legal support ensures your rights as a beneficiary are upheld, protecting the financial foundation that your loved one worked so hard to leave behind.